The Death of Shallow SaaS

Over the past few months, public software stocks have sold off sharply. Some commentators have labeled it a “SaaS-pocalypse.”

That framing is dramatic. It’s also misleading.

SaaS is not dying. But a certain type of SaaS is under real pressure.

What we’re seeing is not the end of software. It’s the repricing of shallow software.

What’s Actually Happening

Public software stocks have sold off sharply this year, with the broader software index entering correction territory.

Three things are driving the selloff:

- AI disruption fears

- Valuation compression

- Seat-based revenue risk

Public market investors are asking a simple question:

If AI agents can perform the work that humans used to perform inside software tools, how many seats are still required?

If a customer needed 20 users before and now needs 8, revenue compresses. That’s not a theoretical risk. That’s math.

At the same time, AI makes it easier to build basic software products. That creates downward pricing pressure on tools that were already lightly differentiated.

This does not affect all SaaS equally.

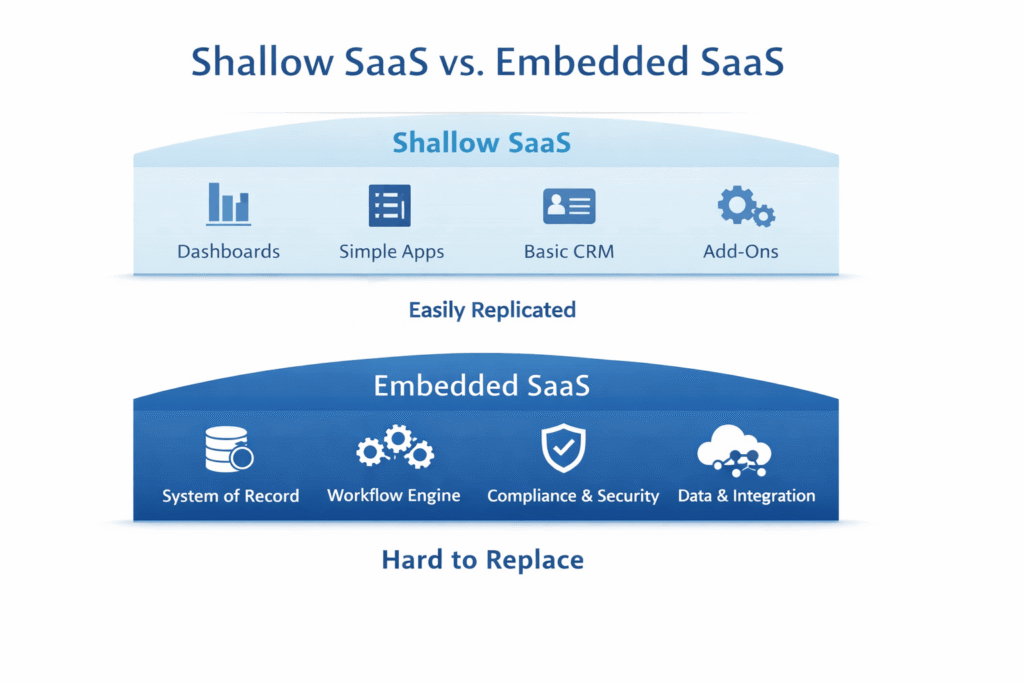

The Real Divide: CRUD vs System of Record

Most SaaS businesses start as CRUD applications.

Create

Read

Update

Delete

In other words, a database with a user interface.

There is nothing wrong with that. But if the value of the product lies primarily in the interface — not in deep workflow ownership — then AI can replicate large portions of it quickly.

The most exposed companies are:

- Thin reporting dashboards

- Resume builders

- Generic workflow tools

- Light marketing automation

- Standalone feature products

- High seat-count productivity tools

If your product is a feature, it can be bundled.

If your product is a UI wrapper, it can be replicated.

If your pricing is seat-based, it can compress

What’s More Durable

The insulated businesses look very different.

- Systems of record (accounting, ERP, payroll, EMR)

- Compliance-driven software

- Infrastructure and security platforms

- Deeply embedded vertical SaaS

- Businesses with proprietary data moats

- Platforms that control money movement

These products have their own workflow. They are not surface-level tools. They sit at the center of operations.

AI is more likely to enhance these platforms than replace them.

As Harvard Business Review has noted in its discussion of competitive advantage in the age of AI, the real defensibility comes from data scale, ecosystem integration, and workflow depth — not from surface-level features. AI amplifies structural advantages. It does not erase them.

The More Relevant Stress Test

You’ll hear a lot about the Rule of 40 in this environment.

Most of the $3m–$10m ARR SaaS companies I work with do not hit the Rule of 40. That’s normal, especially for founder-led businesses that reinvest unevenly or prioritize growth over margin.

Many founders in this position speak with a SaaS business broker to understand how buyers are evaluating durability, defensibility, and cash flow in the current market.

The more relevant question right now is not whether you hit a formula.

It’s this:

If growth slows by 10–15 points, does your business still produce meaningful cash flow?

AI pressure, pricing compression, or longer sales cycles can easily shave growth rates.

If EBITDA disappears when growth slows, that’s a risk.

If EBITDA improves or holds steady when growth moderates, that’s durability.

That’s what buyers are underwriting today.

Not just growth.

Not just profitability.

But resilience if growth normalizes.

It seems like we always come back to the value of low churn.

What Buyers Are Underwriting Now (2026)

In the lower middle market ($3m–$10m ARR), buyers are not panicking. But they are more selective.

They are focused on:

- Revenue durability

- Multi-year contracts

- Low churn

- Switching cost

- Integration depth

- Regulatory exposure

- Cash generation

They are discounting:

- High growth without defensibility

- SMB models with weak retention

- Products driven mostly by paid marketing

- Thin feature sets

The gap between embedded SaaS and shallow SaaS is widening.

This Is a Repricing, Not a Collapse

Enterprise software is expensive to build and maintain because of low enterprise risk tolerance. Security, compliance, uptime, integrations, audit trails — none of that disappears because AI writes code faster.

AI improves productivity. It does not eliminate enterprise complexity.

The current market is not saying software has no value. It is saying not all software deserves premium valuations, and the gap between durable platforms and shallow tools is increasingly reflected in SaaS company valuation multiples.

That distinction matters.

The Honest Question for Founders

For founders thinking about durability, defensibility, and long-term value, it’s also worth understanding the typical process for selling a SaaS company and how buyers evaluate risk during an acquisition.

If OpenAI launched a generic AI agent tomorrow, would it:

A) Replace your product?

B) Enhance your product?

C) Need your product’s data and workflow to function?

If the answer is A, defensibility deserves serious attention.

If the answer is C, you likely have something durable.

SaaS is not dead.

Shallow SaaS is under pressure.

And buyers are getting much clearer about the difference.