In the $3–20M SaaS market, valuation tension rarely comes from bad math.

More often, it comes from a shift in context.

I’ve seen situations where a founder receives a thoughtful, well-supported valuation for planning or tax purposes. Months later, when they begin exploring a sale, the live offers don’t match that earlier number. That moment can create friction — not because someone made a mistake, but because the question being answered has changed.

A financial valuation asks:

What is this business worth under a defined set of modeled assumptions?

A transaction asks something slightly different:

What will a buyer actually fund, under real capital constraints, with risk priced and structure negotiated?

Those questions overlap — but they are not identical.

When a company moves from planning mode to transaction mode, additional variables come into play:

- Required return thresholds

- Risk underwriting

- Structural normalization

- Liquidity conditions

- Capital market constraints

In lower middle market SaaS, those variables can materially influence the market-clearing outcome.

The purpose of this article is not to critique financial valuation methodology. It’s to explain why transaction pricing can differ — and why understanding those differences early tends to make the eventual process smoother for founders and their advisors.

Discount Rates and Required IRR: Where the Gap Often Begins

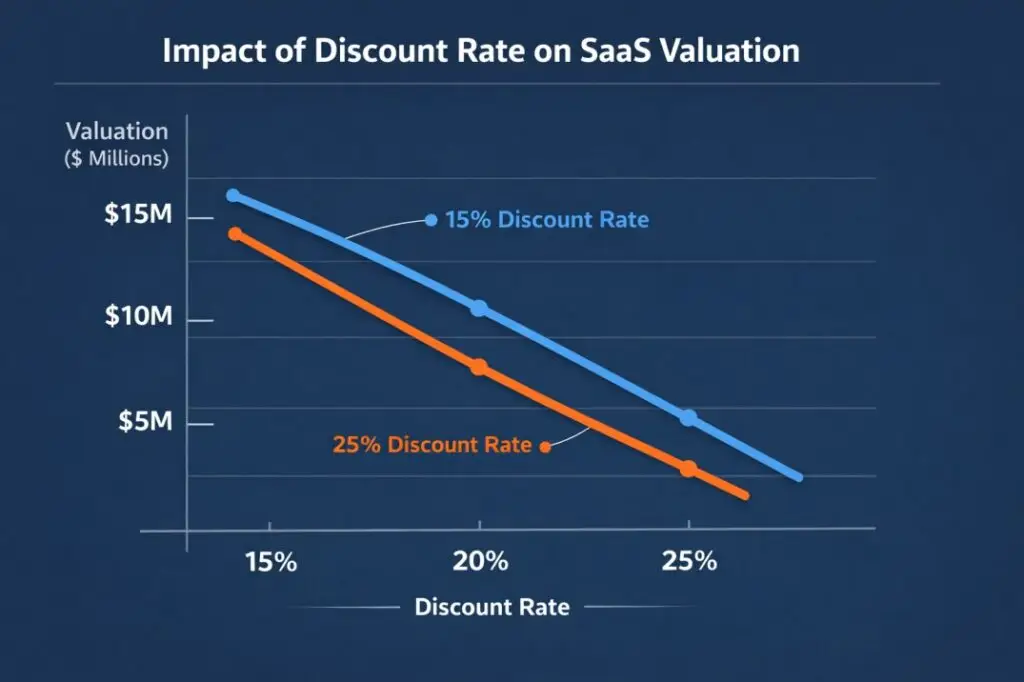

One of the most common sources of divergence between a financial valuation and a live transaction outcome is the discount rate applied to future cash flows.

In many formal valuations for planning or tax purposes, the discount rate is derived from standard methodologies:

- A weighted average cost of capital (WACC)

- CAPM inputs such as beta and equity risk premium

- Industry benchmarks

- Company-specific risk adjustments

For a profitable, growing SaaS business, that analysis may yield a discount rate in the mid-teens—often 12–18%, depending on assumptions.

That framework is coherent and defensible within its purpose.

Transaction buyers, however, are not solving for theoretical fair value. They are solving for the required return on deployed capital.

Private equity funds commonly underwrite to gross IRR targets in the 20–30%+ range. Independent sponsors may require even higher returns, particularly where leverage is constrained. Strategic buyers often face internal capital-allocation hurdles tied to corporate return mandates. All of them apply additional company-specific risk adjustments based on concentration, key-person dependence, churn volatility, and operational scalability.

Even modest differences in discount rate assumptions can materially shift present value. A 15% discount rate and a 25% required return applied to the same projected cash flows will produce very different outcomes.

Both numbers can be technically defensible. They reflect different capital expectations.

In lower middle market SaaS, this difference is amplified by illiquidity. Buyers are committing capital into a single private asset with operational risk. They are not pricing a diversified public security. Required returns tend to reflect that concentration.

When founders move from a valuation prepared for planning purposes to conversations with live buyers underwriting to specific return thresholds, this shift in discount rate philosophy is often the first place expectations begin to diverge.

Founder-Optimized EBITDA vs Institutional-Ready EBITDA

Another source of valuation divergence in lower-middle-market SaaS transactions stems from how future earnings are framed.

Many founder-led SaaS businesses in the $3–10M revenue range are optimized around efficiency and control. They often operate with:

- Lean management layers

- Founder-led sales

- Minimal finance infrastructure

- Below-market executive compensation

- Limited compliance overhead

From a cash flow standpoint, this can yield attractive EBITDA margins. A DCF built on current economics may reasonably project forward performance under the assumption that the structure continues.

Transaction buyers, however, frequently underwrite to a different operating reality.

An institutional buyer is typically not trying to preserve the founder-dependent structure. They are trying to reduce concentration risk and create operational durability. That often means adding management layers designed to de-risk the business over time.

For example, buyers may assume:

- Hiring a VP of Sales so revenue is not dependent on the founder

- Building out a professionalized customer success function to stabilize retention

- Adding finance leadership to improve reporting quality and forecasting accuracy

- Implementing stronger governance and compliance processes to support scale

- Increasing operational oversight to reduce key-person exposure

I’ve seen founders surprised by how quickly buyers model additional overhead — not because the current structure is “wrong,” but because the buyer’s mandate is different.

Institutional capital generally prioritizes predictability and transferability. A founder-operated SaaS company may perform exceptionally well under its existing structure. Still, from a buyer’s perspective, the business must function independently of the founder and withstand scrutiny from lenders and investment committees.

As a result, forward EBITDA margins under institutional ownership may be modeled lower than historical margins under founder ownership.

Because expected future cash flows ultimately drive valuation, these structural normalization assumptions can materially affect pricing.

In practice, this is one of the most common areas where a financial valuation and a live buyer model diverge — not because the spreadsheet is incorrect, but because the assumed ownership structure differs.

When ownership changes, risk tolerance changes — and the cost structure often follows.

Liquidity and Structure: Why Headline Value and Economic Outcome Differ

Another point of confusion arises not from the valuation itself, but from its structure.

A financial valuation typically produces an enterprise value estimate under a defined set of assumptions. That number is useful for planning, negotiation, and scenario modeling.

A transaction term sheet, however, introduces structure.

In lower middle market SaaS transactions, the structure commonly includes:

- Cash at closing

- Earnout components tied to performance

- Rollover equity retained by the founder

- Indemnity escrows

- Working capital adjustments

- Debt-like item reconciliations

Two transactions can share the same headline enterprise value and produce very different economic experiences for the founder.

For example, a $10M enterprise value structured as 95% cash at close carries very different risk than a $10M enterprise value structured as 70% cash at close with the remainder contingent on future performance.

DCF models generally do not capture the behavioral and structural implications of risk-sharing mechanisms like earnouts. Buyers use these tools to manage uncertainty — particularly around the durability of growth, retention stability, and operational scalability.

From a buyer’s perspective, structure is a way to align incentives and hedge risk. From a founder’s perspective, structure directly affects liquidity certainty and personal financial planning.

I’ve seen situations where the headline valuation number attracted attention, but the real negotiation centered on cash at close and earnout probability. In practice, those structural variables often matter more than the initial multiple.

When founders move from valuation discussions to live buyer conversations, this is frequently where the most meaningful gap emerges — not necessarily in the enterprise value itself, but in how much capital changes hands at closing and under what conditions.

Understanding that distinction early tends to reduce friction later in the process.

Growth Assumptions and Risk Underwriting

Growth assumptions are another area where financial valuations and transaction underwriting often diverge.

Most DCF models rely on management projections. Those projections may incorporate:

- Revenue growth rates

- Gross margin stability

- Customer acquisition efficiency

- Net revenue retention

- Operating leverage over time

When thoughtfully constructed, these models can be internally consistent and analytically sound.

Buyers, however, typically re-underwrite those same assumptions through a risk lens.

In lower middle market SaaS transactions, buyers often examine:

- Cohort-level retention durability

- Net revenue retention consistency across customer segments

- Customer concentration within top accounts

- Dependence on specific acquisition channels

- CAC trends and payback stability

- Churn volatility across economic cycles

- Platform or integration dependencies

A DCF may model expected growth based on historical averages and management forecasts. A buyer will often stress-test those assumptions by applying downside scenarios or reducing terminal growth expectations.

Even modest adjustments to:

- Long-term growth rates

- Exit multiple assumptions

- Retention durability

- Gross margin expansion timing

Can materially impact present value.

For example, reducing the assumed terminal growth from 4% to 2%, or making a conservative adjustment to projected net revenue retention, can meaningfully compress valuation under a DCF framework. Buyers frequently apply these adjustments not because they doubt management, but because their capital mandates require underwriting to defensible downside scenarios.

In practice, this is less about disagreement and more about risk tolerance.

Management projections typically reflect what the business is designed to achieve.

Buyer underwriting reflects what the business must withstand.

In lower middle market SaaS — where customer concentration, founder dependence, and market positioning can vary widely — that difference in underwriting philosophy can meaningfully influence transaction pricing.

A Real-World Illustration: When Both Numbers Made Sense

Consider a founder-led SaaS business generating approximately $5M in ARR with EBITDA margins near 28%.

The company had:

- Solid gross margins

- Moderate customer concentration

- Strong product-market fit

- Founder-led sales involvement

- Limited management layering

- Consistent, but not hypergrowth-level expansion

For internal planning purposes, a DCF was prepared using:

- A mid-teens discount rate

- Projected revenue growth based on historical trends

- Stable margin assumptions

- A terminal growth rate consistent with mature SaaS benchmarks

Under those assumptions, the valuation analysis suggested an enterprise value of $11–12 M.

The analysis was internally consistent and defensible given its purpose.

When the company later explored a sale, institutional buyers approached the underwriting differently.

Their model incorporated:

- A required IRR closer to 25%

- Normalization of founder compensation

- Addition of a professional sales leader

- Incremental finance and reporting overhead

- Conservative adjustments to net revenue retention durability

- Lower terminal growth assumptions

The highest market-clearing offer ultimately came in at approximately $8.5M enterprise value, structured with roughly 90% cash at close and a modest performance-based earnout.

At first glance, the gap between $11–12M and $8.5M appears significant.

However, both numbers were rational within their respective frameworks.

The DCF reflected modeled performance under a defined set of assumptions.

The transaction price reflected required returns, structural normalization, liquidity constraints, and live risk underwriting by buyers deploying capital under mandate.

The more important conversation ultimately centered not on the headline gap, but on:

- Liquidity certainty

- Risk transfer

- Institutionalization requirements

- Forward operational independence

The transaction closed cleanly, with high cash at close and limited contingent exposure — which, for the founder, mattered more than the initial headline valuation comparison.

This is not an uncommon scenario in the lower-middle-market SaaS space.

When the valuation purpose shifts from planning to transaction, pricing dynamics shift with it.

When Both Outcomes Are Technically Correct

Situations like the example above are not evidence that one analysis was flawed and the other was “right.”

They reflect that different frameworks were applied to answer different questions.

A financial valuation prepared for planning, tax, or internal shareholder purposes may reasonably assume:

- A discount rate derived from market benchmarks

- Management-projected growth

- Continuity of current operating structure

- A long-term steady-state terminal value

A transaction buyer, by contrast, must underwrite:

- Required return thresholds tied to capital mandates

- Structural normalization to institutional ownership

- Risk concentration and key-person exposure

- Liquidity constraints

- Current debt market conditions

- Downside scenario resilience

Both approaches can be internally coherent.

They operate under different constraints.

Where friction tends to arise is not in the math itself, but in the anchoring of expectations.

Once a founder internalizes a valuation number, it becomes the reference point. When live offers reflect different discount rates, structural assumptions, or liquidity adjustments, it can feel like a disagreement over value — when in reality it is often a disagreement over framework.

That distinction matters.

In practice, the most constructive approach is to clarify early:

- What purpose does the valuation serve?

- Which assumptions are sensitive

- How institutional buyers may re-underwrite growth and margins

- How structure affects economic outcome

When those distinctions are discussed before launching a sale process, alignment improves, and emotional friction decreases.

In my experience, founders and their advisors are best served when the conversation moves from:

“What is the theoretical value?”

To:

“What would a buyer need to see — and require — to fund this at closing?”

That shift tends to produce smoother processes and fewer surprises.

Conclusion: Clarity Before Process

Financial valuations are essential tools. They serve meaningful purposes in tax planning, estate structuring, shareholder alignment, and strategic decision-making.

Transaction pricing, however, introduces additional variables:

- Required return thresholds

- Structural normalization

- Risk underwriting

- Liquidity considerations

- Capital market conditions

- Deal structure mechanics

In lower middle market SaaS, these factors can materially influence what ultimately clears the market.

When founders move from planning discussions to live buyer conversations without adjusting the valuation framework, friction often follows. Not because anyone acted in bad faith — but because the purpose of the analysis changed.

Understanding that shift early tends to protect everyone involved:

- The founder avoids anchoring to a number divorced from transaction dynamics.

- The advisor preserves credibility by framing the valuation context appropriately.

- The process unfolds with clearer expectations around structure, liquidity, and risk allocation.

In practice, the most productive conversations occur before a formal process begins — when assumptions can be stress-tested against real buyer behavior and capital constraints.

For advisors working with SaaS companies in the $3–20M range, that alignment often makes the difference between a smooth closing and an unnecessarily contentious negotiation.

If you advise SaaS businesses and would like to compare notes on current transaction dynamics in this market segment, I’m always open to a thoughtful conversation.

For a broader overview of how buyers value software companies, see: SaaS and Software Company Valuation.