The Illusion of Buyers When Selling a SaaS Company

Many founders believe there are thousands of buyers for their company.

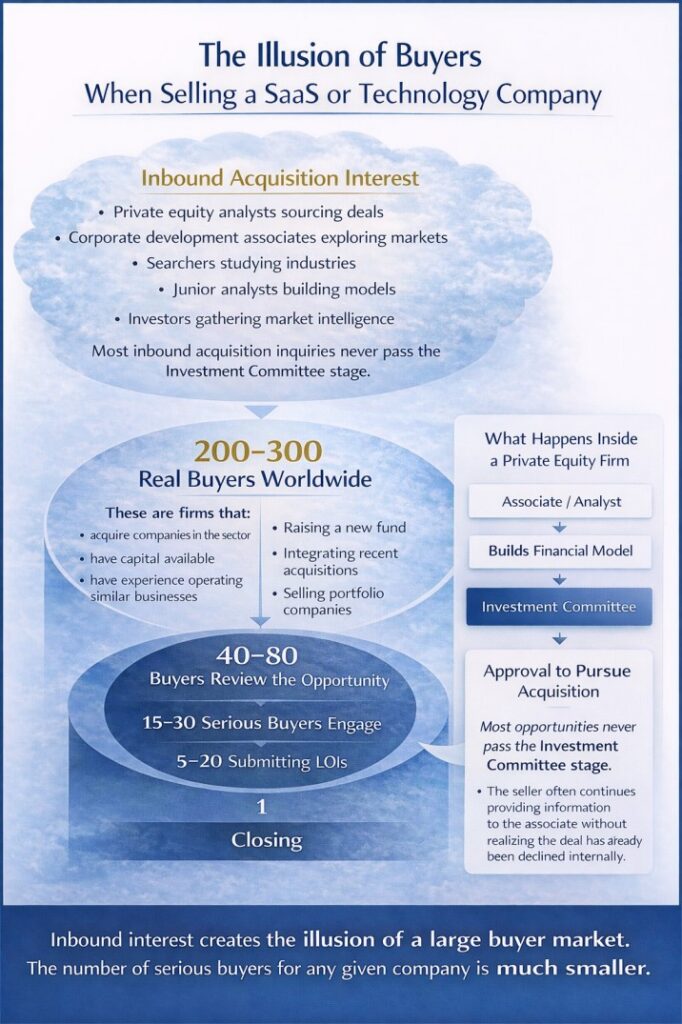

They receive inbound emails from investors, private equity associates, and corporate development professionals asking to “learn more about the business.”

Introductory calls happen. Financial information is requested. Sometimes, a detailed financial model is even built.

It can feel like there is an enormous demand for the company.

In reality, much of this activity represents market screening rather than acquisition intent.

Understanding this difference is important for founders considering how to sell a SaaS company.

Inbound Interest Often Creates a False Signal

Many private equity firms and strategic buyers continuously scan the market for opportunities.

Junior analysts and associates are responsible for sourcing deals. Their job often includes:

- contacting founders in target industries

- gathering financial information

- building three-statement financial models

- preparing internal investment memos

From the founder’s perspective, this can appear to be a serious acquisition interest.

But inside the investment firm, the opportunity may still be at the very earliest screening stage.

Most opportunities never progress beyond this point.

The Step Founders Rarely See: The Investment Committee

Inside most investment firms, acquisitions follow an internal decision process.

Associate or Analyst

↓

Financial Model and Initial Review

↓

Investment Committee Discussion

↓

Approval to Pursue Acquisition

The investment committee is typically composed of the firm’s partners. They decide whether the opportunity fits the firm’s mandate.

If the committee declines to pursue the deal, the process stops immediately.

The founder may never know this happened.

They may continue sending information to the analyst without realizing the opportunity has already been rejected internally.

This is one reason why inbound acquisition interest can create the illusion of a large buyer market.

The Real Buyer Pool Is Much Smaller

When founders imagine potential buyers, they often think about a large universe of investors:

Private equity firms

Strategic technology companies

Family offices

Search funds

Entrepreneurs looking to acquire businesses

While thousands of organizations exist in these categories, only a fraction will realistically consider a specific company.

For most opportunities, the number of serious potential buyers may be roughly 200–300 firms nationwide.

Even within this group, not every buyer is actively pursuing acquisitions at any given time.

Some firms may be:

- raising a new fund

- integrating recently acquired companies

- selling portfolio companies

- focusing on different sectors

- reviewing other transactions

This means the number of buyers actively evaluating opportunities may be far smaller.

How the Buyer Funnel Actually Works

When a company goes to market, the process usually resembles a funnel.

Approximately 200–300 potential buyers may exist in the sector.

From that group:

40–80 buyers may briefly review the opportunity.

15–30 buyers may engage in more serious discussions.

5–20 buyers may submit Letters of Intent (LOIs).

And ultimately, one buyer closes the transaction.

This is why experienced advisors focus on reaching the right buyers and ensuring several of them evaluate the opportunity at the same time.

Competition among qualified buyers is what creates leverage in the sale process.

Why Random Inbound Opportunities Receive Less Attention

Professional buyers evaluate a large number of opportunities every week.

Because of this, they often prioritize opportunities that come from trusted sources, such as:

- experienced M&A advisors

- industry operators they already know

- portfolio company executives

- long-standing professional relationships

Random inbound opportunities typically receive less attention, especially when buyers are already reviewing several deals.

This is another reason why the perceived buyer market often appears larger than the actual market of serious acquirers.

Preparation Matters More Than Exposure

Many founders assume the goal when selling a company is to show the opportunity to as many buyers as possible.

In practice, the objective is more focused.

The goal is to identify the buyers most likely to value the business and ensure they evaluate the opportunity within a structured process.

Companies that are well-prepared tend to attract the greatest serious attention and interest. Preparation includes:

- clear financial statements

- credible valuation expectations

- transparent discussion of risks

- clear explanation of growth opportunities

These factors strongly influence how buyers evaluate opportunities and how valuations are determined.

For a deeper discussion of how buyers evaluate SaaS companies, see our page on how SaaS metrics shape valuation.

Final Thoughts

Inbound acquisition interest can make the buyer market appear larger than it actually is.

But most early conversations represent screening activity, not serious acquisition intent.

The number of qualified buyers for any given company is typically much smaller than founders expect.

Understanding this dynamic is important for founders considering when and how to sell.

If you are evaluating whether now is the right time to sell, you may also find it helpful to review our guide on thinking about selling a SaaS business.